|

117 |

|

|

118 |

|

|

132 |

|

|

135 |

|

|

136 |

|

|

136 |

|

|

137 |

|

|

137 |

|

|

138 |

|

|

139 |

|

|

140 |

|

|

143 |

|

|

145 |

|

|

146 |

|

|

148 |

|

|

149 |

|

|

151 |

|

|

151 |

|

|

152 |

|

|

153 |

|

|

154 |

|

|

155 |

|

|

157 |

|

|

159 |

|

|

159 |

|

|

163 |

|

|

164 |

|

|

164 |

|

|

165 |

|

|

165 |

|

|

166 |

|

|

167 |

|

|

168 |

|

|

168 |

|

|

168 |

|

|

169 |

|

|

37. Critical Accounting Judgements and Key Sources of Estimation and Uncertainty |

170 |

|

38. Disclosures according to section 161 German Stock Corporation Act (AktG) |

170 |

AIXTRON SE (“Company”) is incorporated as a European Company (Societas Europaea) under the laws of the Federal Republic of Germany. The Company is domiciled at Dornkaulstraße 2, 52134 Herzogenrath, Germany. AIXTRON SE is registered in the commercial register of the District Court (“Amtsgericht”) of Aachen under HRB 16590.

The consolidated financial statements of AIXTRON SE and its subsidiaries (“AIXTRON“ or “Group“) have been prepared in accordance with, and fully comply with

• International Financial Reporting Standards (IFRS) as adopted for use in the European Union; and

• the requirements of Section 315e of HGB (German Commercial Law).

AIXTRON is a leading provider of deposition equipment to the semiconductor industry. The Group's technology solutions are used by a diverse range of customers worldwide to build advanced components for electronic and opto-electronic applications based on compound, silicon, or organic semiconductor materials. Such components are used in fiber optic communication systems, wireless and mobile telephony applications, optical and electronic storage devices, computing, signaling, and lighting, displays, as well as a range of other leading-edge technologies.

These consolidated financial statements have been prepared by the Executive Board and have been submitted to the Supervisory Board at its meeting held on February 27, 2023 for approval and publication.

Companies included in consolidation are AIXTRON SE, and companies controlled by AIXTRON SE. The balance sheet date of all consolidated companies is December 31. A list of all consolidated companies is shown in note 32.

The consolidated financial statements are presented in Euro (EUR). The amounts are rounded to the nearest thousand Euro (EUR thousand).

The financial statements have been prepared on the historical cost basis, except for the revaluation of certain financial instruments.

The preparation of financial statements in conformity with IFRS, as they are to be applied in the EU, requires management to make estimates and judgements that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the balance sheet date and the reported amounts of income and expenses during the reported period. Actual results may differ from these estimates.

The estimates and judgements are reviewed on an ongoing basis. Revisions to accounting estimates and judgements are recognized in the period in which the estimate is revised if this revision affects only that period, or in the period of the revision and future periods if the revision affects both current and future periods. Estimates and judgments which have a significant effect on the Group’s financial statements are described in note 37.

The accounting policies set out below have been applied consistently to all periods presented in these consolidated financial statements.

The accounting policies have been applied consistently by each consolidated company.

The consolidated financial statements incorporate the financial statements of the Company and entities controlled by the Company (its subsidiaries) made up to 31 December each year. Control is achieved when the Company:

The Company reassesses whether or not it controls an investee if facts and circumstances indicate that there are changes to one or more of the three elements of control listed above.

Entities over which AIXTRON SE has control are treated as subsidiaries (see note 32). The results of subsidiaries are included in the consolidated financial statements from the date that control commences until the date that control ceases.

All intercompany income and expenses, transactions and balances have been eliminated in the consolidation.

The consolidated financial statements have been prepared in Euro (EUR). In the translation of financial statements of subsidiaries outside the Euro-Zone the local currencies are also the functional currencies of those companies. Assets and liabilities of those companies are translated to EUR at the exchange rate as of the balance sheet date. Income and expenses are translated to EUR at average exchange rates for the year or at average exchange rates for the period between their inclusion in the consolidated financial statements and the balance sheet date. Net equity is translated at historical rates. The differences arising on translation are disclosed in the consolidated statement of changes in equity.

Exchange gains and losses resulting from fluctuations in exchange rates in the case of foreign currency transactions are recognized in the income statement in „other operating income“ or „other operating expenses“.

Items of property, plant and equipment are stated at cost, plus ancillary charges such as installation and delivery costs, less accumulated depreciation (see below) and impairment losses (see accounting policy (J)).

Costs of internally generated assets include not only costs of material and personnel, but also a share of directly attributable overhead costs, such as employee benefits, delivery costs, installation, and professional fees.

Where parts of an item of property, plant and equipment have different useful lives, they are depreciated as separate items of property, plant and equipment.

AIXTRON recognizes in the carrying amount of an item of property, plant and equipment the cost of replacing components or enhancement of such an item when that cost is incurred if it is probable that the future economic benefits embodied in the item will flow to the Group and the cost of the item can be measured reliably. All other costs such as repairs and maintenance are expensed as incurred.

Government grants related to the acquisition or manufacture of owned assets are deducted from original cost at the date of capitalization.

Depreciation is charged on a straight-line basis over the estimated useful lives of each part of an item of property, plant and equipment. Useful lives, depreciation method and residual values of property, plant and equipment are reviewed at the year-end date or more frequently if circumstances arise which are indicative of a change. The estimated useful lives are as follows:

The Group only has contracts in which it is the lessee.

AIXTRON assesses whether a contract is, or contains, a lease, at inception of the contract. The Group recognizes a lease asset and a corresponding lease liability with respect to all lease arrangements in which it is the lessee, except for short-term leases (defined as leases with a lease term of 12 months or less) and leases of low value assets (such as tablets and personal computers, small items of office furniture and telephones). For these leases, the Group recognizes the lease payments as an operating expense on a straight-line basis over the term of the lease unless another systematic basis is more representative of the time pattern in which economic benefits from the leased assets are consumed.

AIXTRON recognizes a leased asset and a lease liability at the lease commencement date. The leased asset is initially measured at cost, which comprises the initial amount of the lease liability adjusted for any lease payments made at or before the commencement date, plus any initial direct costs incurred and an estimate of costs to dismantle and remove the underlying asset or to restore the underlying asset or the site on which it is located, less any lease incentives received.

The leased asset is subsequently depreciated using the straight-line method from the commencement date to the earlier of the end of the useful life of the asset or the expected end of the lease term. The estimated useful lives of leased assets are determined on the same bases as those of property, plant and equipment. In addition, the leased asset is periodically tested and reduced by impairment losses, if any, and adjusted for certain remeasurements of the lease liability.

The right-of-use assets are presented in property, plant and equipment, and leased assets in the consolidated statement of financial position.

The lease liability is initially measured at the present value of the lease payments that are not paid at the commencement date, discounted using the interest rate implicit in the lease or, if that rate cannot be readily determined, the company’s incremental borrowing rate.

Lease payments included in the measurement of the lease liability comprise fixed payments, less any lease incentives and variable lease payments that depend on an index or rate, initially measured using the index or rate at the commencement date.

The lease liabilities are included in other non-current payables and other current liabilities in the consolidated statement of financial position.

The lease liability is measured at amortized cost using the effective interest method. It is remeasured when there is a change in future lease payments arising from a change in index or rate, or if the company changes its assessment of whether it will exercise a purchase, extension or termination option. When the lease liability is remeasured in this way, a corresponding adjustment is made to the carrying amount of the leased asset, or is recorded in profit or loss if the carrying amount of the leased asset has been reduced to zero.

The Group did not make any such adjustments during the periods presented.

Business combinations are accounted for by applying the purchase method.

Goodwill is stated at cost less any accumulated impairment loss. Goodwill is allocated to cash-generating units and is tested at least once per year for impairment (see accounting policy (J)).

Expenditure on research activities, undertaken with the prospect of gaining new technical knowledge and understanding using scientific methods, is recognized as an expense as incurred.

Expenditure on development comprises costs incurred with the purpose of using scientific knowledge technically and commercially. As not all criteria of IAS 38 are met AIXTRON does not capitalize such costs.

Other intangible assets that are acquired are stated at cost less accumulated amortization (see below) and impairment losses (see accounting policy (J)).

Intangible assets acquired through business combinations are stated at their fair value at the date of purchase.

Expenditure on internally generated goodwill, trademarks and patents is expensed as incurred.

Subsequent expenditure on capitalized intangible assets is capitalized only when it increases the future economic benefits embodied in the specific asset to which it relates. All other expenditure is expensed as incurred.

Amortization is charged on a straight-line basis over the estimated useful lives of intangible assets, except for goodwill. Goodwill has a useful life which is indefinite and is tested annually in respect of its recoverable amount. Other intangible assets are amortized from the date they are available for use. Useful lives and residual values of intangible assets are reviewed at the year-end date or more frequently if circumstances arise which are indicative of a change.

The estimated useful lives are as follows:

Financial assets are classified into the following specific categories:

The classification depends on the nature and purpose of the financial assets and is determined at the time of initial recognition.

AIXTRON did not have any financial assets in this category during the periods covered by this report.

Financial assets are measured at amortized cost as they are held within a business model to collect contractual cash flows and these cash flows consist solely of payments of principal and interest on the principal amount outstanding.

All financial assets not classified as measured at amortized cost or FVTOCI under IFRS 9 are measured at fair value through profit and loss (FVTPL).

Financial assets at FVTPL are measured at fair value at the end of each reporting period, with any fair value gains or losses recognized in profit or loss. The gain or loss including dividends earned on financial asset and is included in profit and loss account and in note 5 or 6 respectively. Fair value is determined in accordance with IFRS 13.

Trade receivables and other receivables are measured at amortized cost as they are held within a business model to collect contractual cash flows and these cash flows consist solely of payments of principal and interest on the principal amount outstanding.

The Group recognizes a loss allowance for expected credit losses (ECL) on trade receivables and contract assets. The amount of expected credit losses is updated at each reporting date to reflect changes in credit risk since initial recognition of the respective financial instrument. The Group always recognizes lifetime ECL for trade receivables, and contract assets. The expected credit losses on these financial assets are estimated using a provision matrix based on the Group’s historical credit loss experience, adjusted for factors that are specific to the debtors, general economic conditions and an assessment of both the current as well as the forecast direction of conditions at the reporting date, including time value of money where appropriate.

For all other financial instruments, the Group recognizes lifetime ECL when there has been a significant increase in credit risk since initial recognition. However, if the credit risk on the financial instrument has not increased significantly since initial recognition, the Group measures the loss allowance for that financial instrument at an amount equal to 12‐month ECL. Lifetime ECL represents the expected credit losses that will result from all possible default events over the expected life of a financial instrument. In contrast, 12‐month ECL represents the portion of lifetime ECL that is expected to result from default events on a financial instrument that are possible within 12 months after the reporting date.

Cash and cash equivalents comprise cash on hand and deposits with banks with a maturity of less than three months at inception.

Equity instruments, including share capital, issued by the Group are recorded at the proceeds received, net of direct issue costs.

Financial liabilities are classified as either financial liabilities “at FVTPL” or "at amortized cost".

AIXTRON did not have any financial liabilities in this category during the periods covered by this report.

Other financial liabilities, including trade payables, are measured at amortized cost.

The Group’s activities expose it to the financial risks of changes in foreign exchange currency rates (see note 25). AIXTRON may use foreign exchange forward contracts to hedge these exposures. AIXTRON does not use derivative financial instruments for speculative purposes. The use of financial derivatives is governed by policies approved by the Executive Board, which provide written principles on the use of financial derivatives.

AIXTRON did not have any derivative financial instruments in the periods covered by this report.

Inventories are stated at the lower of cost and net realizable value. Net realizable value is the estimated selling price in the ordinary course of business, less the estimated cost of completion and selling expenses. Cost is determined using weighted average cost.

The cost includes expenditures incurred in acquiring the inventories and bringing them to their existing location and condition. In the case of work in progress and finished goods, cost includes direct material and production cost, as well as an appropriate share of overheads based on normal operating capacity. Scrap and other wasted costs are expensed on a periodic basis either as cost of sales or, in the case of beta tools as research and development expense.

Allowance for slow moving, excess and obsolete, and otherwise unsaleable inventory is recorded based primarily on either the estimated forecast of product demand and production requirement or historical usage. When the estimated future demand is less than the inventory, AIXTRON writes down such inventories.

Operating result is stated before finance income, finance expense and tax.

Goodwill purchased as part of a business acquisition is tested at least annually for impairment, irrespective of whether there is any indication of impairment. For impairment test purposes, the goodwill is allocated to cash-generating units. Impairment losses are recognized to the extent that the carrying amount exceeds the higher of fair value less costs of disposal or value in use of the cash-generating unit. Details of impairment test are shown in note 12.

Property, plant and equipment as well as other intangible assets are tested for impairment, where there is any indication that the asset may be impaired. The Group assesses at the end of each period whether there is an indication that an asset may be impaired. Impairment losses on such assets are recognized, to the extent that the carrying amount exceeds both the fair value that would be obtainable from a disposal in an arm’s length transaction, and the value in use.

In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments and the risks associated with the asset.

Impairment losses are reversed if there has been a change in the estimates used to determine the recoverable amount. Reversals are made only to the extent that the carrying amount of the asset does not exceed the carrying amount that would have been determined if no impairment loss had been recognized.

An impairment loss in respect of goodwill is not reversed.

Basic earnings per share are computed by dividing net income (loss) by the weighted average number of issued common shares for the year. Diluted earnings per share reflect the potential dilution that could occur if options issued under the Company’s stock option plans were exercised unless such exercises had an anti-dilutive effect.

Obligations for contributions to defined contribution pension plans are recognized as an expense in the income statement as incurred.

Stock Option Programs

The stock option programs from 2007 and 2012 allow members of the Executive Board, management, and employees of the Group to acquire shares of AIXTRON SE. The contractual terms of these share programs are presented in note 22. These stock option programs are accounted for according to IFRS 2 for equity-settled share-based payment transactions. The fair value of options granted is recognized as personnel expense with a corresponding increase in additional paid-in capital. The fair value is calculated at grant date and spread over the period during which the employees become unconditionally entitled to the options. The fair value of the options granted is measured using a mathematical model, taking into account the terms and conditions upon which the options were granted. The vesting conditions relate to a service condition and a market condition in relation to the share price of AIXTRON SE. In the calculation of the personnel expense options forfeited during the performance period are taken into account.

Executive Board remuneration system at AIXTRON SE consists long-term variable remune-ration incentives (LTI) granted in shares of AIXTRON SE. These equity-settled share-based payments are measured at fair value of the equity instruments at the grant date. The fair value of the shares granted is measured using a mathematical model, taking into account the terms and conditions upon which the shares were granted. Further details regarding the equity-settled share-based transactions are set out in note 22 and 31.

The fair value determined at the grant date of the equity-settled share-based payments is expensed on a straight-line basis over the performance period, based on the Group’s estimate of the number of equity instruments expected to vest. For non-market-based vesting conditions, the Group reviews its estimate of number of equity instruments at each reporting date during vesting period. The impact of the revision of the original estimates, if any, is recognized in profit or loss and a corresponding adjustment is recognized to equity.

A provision is recognized when the Group has a present legal or constructive obligation as a result of a past event, and it is probable that an outflow of economic benefits will be required to settle this obligation. If the effect is material, provisions are determined by discounting the expected future cash flows at a pre-tax interest rate that reflects current market assessments of the time value of money and, where appropriate, the risks associated with the liability.

The Group normally offers one- or two-year warranties on all of its products. Warranty expenses generally include cost of labor, material and related overhead necessary to repair a product free of charge during the warranty period. The specific terms and conditions of those warranties may vary depending on the equipment sold, the terms of the contract and the locations from which they are sold. The Group establishes the costs that may be incurred under its warranty obligations and records a liability in the amount of such costs at the time revenue is recognized.

Factors affecting the warranty obligation include the historical and expected number of warranty claims and the estimated cost per warranty claim.

The Group accrues warranty cost for systems shipped based upon historical experience. The Group periodically assesses the adequacy of its recorded warranty provisions and adjusts the amounts as necessary.

Extended warranties, beyond the normal warranty periods, are treated as maintenance services in accordance with note 2(N) below.

A provision for onerous contracts is recognized when the expected economic benefits to be derived by the Group from a contract are lower than the unavoidable cost of meeting its obligations under the contract. The amount recognized as a provision is determined as the excess of the unavoidable costs of meeting the obligations under the contract over the economic benefits expected to be received. Before making that provision any impairment loss that has occurred on assets dedicated to that contract are recognized. The provision is discounted to present value if the adjustment is material.

A restructuring provision is recognized when the Group has developed a detailed formal plan for the restructuring and the parties concerned have been informed. The measurement of restructuring provision includes only the direct expenditures arising from the restructuring, which are those amounts that are both necessarily entailed by the restructuring and not associated with the ongoing activities of the entity.

AIXTRON enters contracts with customers for goods and services, including combinations of goods and services. Contracts are usually for fixed prices and do not offer any unilateral right of return to the customer.

Revenue is generated from the following major sources:

Revenue is recognized when the Group satisfies a performance obligation in contracts with its customers by transferring control of promised goods or services to the customer and it is probable that the economic benefits associated with the transaction will flow to the entity.

The sale of equipment involves acceptance tests at AIXTRON ́s production facility. After successful completion of this test, the equipment is dismantled and packaged for shipment.

Revenues from the sale of products that have been demonstrated to meet product specification requirements are recognized at a point in time upon shipment to the customer if full acceptance tests have been successfully completed at the AIXTRON production facility and control has passed to the customer and the customer can benefit from the product either on its own or with other resources that are readily available.

Upon arrival at the customer site the equipment is reassembled and installed, which is a service generally performed by AIXTRON engineers. Revenue relating to the installation of the equipment is recognized at the point in time when AIXTRON has fulfilled its performance obligations under the contract and control of the goods has passed to the customer.

Revenue related to equipment where meeting the product specification requirements has not yet been demonstrated or the customer cannot benefit from the product either on its own or with other resources that are readily available, or where specific rights of return have been negotiated, is recognized only at the point in time when the customer finally accepts the equipment and has control.

Revenue related to spares is recognized at the point in time at which the customer obtains control of the goods, generally at the point of delivery.

Revenue related to services such as repair works is recognized at the point in time as the customers accepts the equipment at this point.

Revenue for services such as extended warranty, is recognized over time during the period in which it is provided. No revenue was generated from extended warranty in the fiscal year.

As part of the payment terms, AIXTRON does not grant any general right of return, cash discount, credit notes or other sales incentives. Generally, payment terms for advance payments and customer invoices are short-term and contracts do not include a financing component.

The consideration from contracts which include combinations of different performance obligations such as equipment, spares and services is allocated to each performance obligation in an amount that depicts the amount of consideration to which the Group expects to be entitled in exchange for transferring the goods or services to the customer. Discounts from list price are proportionately allocated to each performance obligation. The transaction price is allocated to each performance obligation based on a relative stand-alone selling price basis. As the stand-alone selling prices are usually not directly observable, AIXTRON uses the expected cost plus a margin approach to estimate the stand-alone selling price.

The portion of equipment revenue related to installation services is determined based on either the method described above or, if the Group determines that there may be a risk that the economic benefits of installation services may not flow to the Group, the portion of the contract amount that is due and payable upon completion of the installation.

Contract assets may arise for contracts with different performance obligations if the revenue recognized exceed the amounts for received advance payments and customer invoices (see note 16).

Cost of sales includes such direct costs as materials, labor, and related production overheads.

Research and development costs are expensed as incurred. Costs of beta tools which do not qualify to be recognized as an asset are expensed as research and development costs.

Project funding received from governments (e.g. state funding) is recorded in other operating income, if the research and development costs are incurred and provided that the conditions for the funding have been met.

Payments made under leases for assets which have not been capitalized are recognized as expense on a straight-line basis over the term of the lease.

Government grants awarded for project funding are recorded in other operating income if the research and development costs are incurred and provided that the conditions for the funding have been met. Government grants awarded to support continued employment where work is not allowed are recorded as a reduction in the related expense, as this presents the underlying reason for the grant better.

The tax expense represents the sum of the current and deferred tax.

A deferred tax asset is recognized only to the extent that it is probable that future taxable profits can be set off against timing differences and tax losses carried forward or taxable temporary differences exist. Deferred tax assets are reduced to the extent that it is no longer probable that the related tax benefit can be realized. The recoverability of deferred tax assets is reviewed at least annually.

Deferred tax assets and liabilities are recorded for temporary differences between tax and commercial balance sheets and for losses brought forward for tax purposes as well as for tax credits of the companies included in consolidation. Deferred tax assets and liabilities shall be measured at the tax rates that are expected to apply to the period when the asset is realized or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted by the end of the reporting period.

Current income taxes for the current and prior periods are recognized as a liability to the extent that they have not yet been paid. If the amount attributable to the current and prior periods and already paid exceeds the amount due for those periods, the difference is recognized as an asset. The amount of the expected tax liability or tax receivable reflects the best estimate of the amount, considering tax uncertainties, when applicable.

The Group evaluates income tax uncertain treatments on a regular basis. In making this assessment, the Group assumes that a tax authority will review the matter in question and that it has all the relevant information to do so. If it is probable that an uncertain tax treatment will not be accepted by the tax authorities, the best estimate (expected value or most likely value of the tax uncertainty) is used to determine the impact and a tax liability is recognized or, in the case of existing loss carryforwards, the deferred tax attributable to them is reduced accordingly.

An operating segment is a component of the Group that is engaged in business activities and whose operating results are reviewed regularly by the Chief Operating Decision Maker, which AIXTRON considers to be its Executive Board, to make decisions about resources to be allocated to the segment and assess its performance and for which discrete financial information is available. AIXTRON has only one reportable segment.

Accounting standards applied in segment reporting are in accordance with the general accounting policies as explained in this section.

Cash flows from operating activities are determined using the indirect method.

Cash flows from taxes are allocated to operating activities.

Cash flows from other financial assets (fund investments) are presented in cash flow from investing activities as the assets are not traded for trading purposes. As the assets are not traded for trading purposes, it is more appropriate to present them in the cash flow from investing activities as this gives a better insight into the financial position. In the previous year, cash flows from fund investments were reported under cash flow from operating activities. For 2021, EUR 79,862 thousand was reclassified from cash flow from operating activities to cash flow from investing activities.

In the current year, the Group has applied the below amendments to IFRS standards and interpretations issued by the International Accounting Standards Board (IASB) that are effective for an annual period that begins on or after 1 January 2022. Their adoption has not had any material impact on the disclosures or on the amounts reported in these consolidated financial statements.

At the date of authorization of these consolidated financial statements, the Group has not applied following new and revised standards and interpretations which have been issued but are not yet effective. AIXTRON does not expect that the adoption of these standards will have a material impact on the financial statements of the Group in future periods.

1) Initial application to annual reporting periods beginning on or after 1 January 2023.

2) Initial application to annual reporting periods beginning on or after 1 January 2024

3) The effective date of the amendments has yet to be set by the Board.

4) EU endorsement is still pending.

IFRS 8 requires operating segments to be identified on the basis of internal reports about components of the Group that are regularly reviewed by the Executive Board, as chief operating decision maker, in order to allocate resources to the segments and to assess their performance.

In the period 2021 to 2022 the Executive Board regularly reviewed financial information to allocate resources and assess performance only on a consolidated Group basis since the various activities of the Group are largely integrated from an operational perspective. In accordance with IFRS, AIXTRON has only one reportable segment.

The Group’s reportable segment is based around the category of goods and services provided to the semiconductor industry

Revenues are recognized as disclosed in note 2 (N).

Reversals of impairment allowances are included in other operating income as described in note 5.

The accounting policies of the reportable segment are identical to the Group’s accounting policies as described in note 2. Segment profit represents the profit earned by the segment without the allocation of investment revenue, finance costs and income tax expense. This is the measure reported to the Executive Board for the purpose of resource allocation and assessment of performance.

The transaction price allocated to (partially) unsatisfied performance obligations at 31 December 2022 is EUR 351.8 million (31 December 2021: EUR 214.6 million). Management expects that approximately 87% of the transaction price allocated to the unsatisfied contracts as of the year ended 2022 will be recognized as revenue during 2023. The remaining amount will be recognized during the next fiscal year.

For the purpose of monitoring segment performance and allocating resources all assets other than tax assets, cash and cash equivalents and other financial assets are treated as allocated to the reportable segment. All liabilities are allocated to the reportable segment apart from tax liabilities and post-employment benefit liabilities.

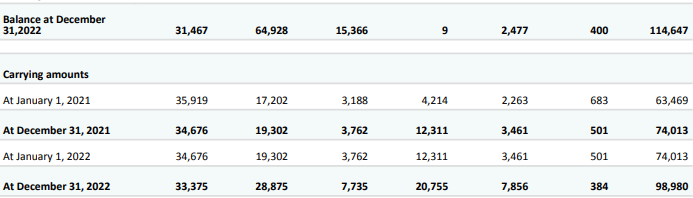

Additions and changes to property, plant and equipment, to goodwill and to intangible as-sets, and the depreciation and amortization expenses are given in notes 11 and 12. Other non-current financial assets were unchanged during 2022 compared to previous year (decreased by EUR 59,8 million during 2021).

Information concerning other material items of income and expense for personnel expenses and R&D expenses can be found in notes 7 and 4.

The Group’s revenue from continuing operations from external customers and information about its non-current assets by geographical location are detailed below. Revenues from external customers are attributed to individual countries based on the country in which it is expected that the products will be used.

Sales from external customers attributed to Germany, AIXTRON’s country of domicile, and to other countries which are of material significance are as follows:

Revenues from all countries outside Germany were EUR 443.906 thousand and EUR 391.844 thousand for the years 2022 and 2021 respectively.

In 2022 no customer accounted for more than 10% of Group revenue. During 2021 sales to one customer represented 12.1% of Group revenue, with no other customer exceeding 10%.

Non-current assets exclude deferred tax assets, financial instruments, post-employment benefit assets and rights arising under insurance contracts.

Research and development costs, before deducting project funding received which is included in other operating income, were EUR 57.726 thousand and EUR 56.809 thousand for the years ended December 31, 2022 and 2021 respectively.

After deducting project funding received and not repayable, net expenses for research and development were EUR 52.424 thousand and EUR 47.876 thousand for the years ended December 31, 2022 and 2021 respectively.

The project funding received amounting to EUR 5.303 thousand (2021: EUR 8.933 thousand) are government grants.

In addition, EUR 15 thousand (2021: EUR 638 thousand) government grants were deducted from the carrying amount of an asset in property, plant and equipment. The reduced depreciation is attributable to research and development.

The amounts for research and development funding are government grants.

In 2022 exchange gains of EUR 2,794 thousand were recognized in profit or loss (2021: gain EUR 1,160 thousand) (see also note 6).

Compensation received in 2022 of EUR 209 thousand (2021: EUR 10 thousand) is an insurance claim for damages incurred during shipment of goods.

In 2022 the gain on disposal of assets amounted to EUR 22 thousand (2021: EUR 20 thousand).

The net loss of EUR 1,047 thousand in 2022 arose on financial assets required to be measured at FVTPL (2021: loss EUR 708 thousand). The amount includes realized losses of EUR 277 thousand (2021: EUR 49 thousand) and unrealized losses of EUR 770 thousand (2021: EUR 659 thousand)

The following table shows income tax expenses and income recognized in the consolidated income statement:

The income/loss before income taxes and income tax expense and income relate to the following regions:

The Group’s effective tax rate is different from the German statutory tax rate of 32.80% (2021: 32.80%) which is based on the German corporate income tax rate (incl. solidarity surcharge) and trade tax.

The following table shows the reconciliation from the expected to the reported tax expense:

In addition to the amount charged to profit or loss, the following amounts relating to tax have been recognized in other comprehensive income (OCI):

As of December 31, 2022 the current tax receivable and payable, arising because the amount of tax paid in the current or in prior periods was either too high or too low, are EUR 2,804 thousand (2021: EUR 2,363 thousand) and EUR 2,439 thousand (2021: EUR 9,729 thousand) respectively.

Depreciation expense amounted to EUR 7,674 thousand for 2022 and EUR 7,843 thousand for 2021 respectively.

During each fiscal year, asset useful lives and residual values are reviewed in accordance with IFRS. In 2022 the effect of the changes in asset useful lives and residual values has been to decrease the depreciation expense by EUR 933 thousand compared with the depreciation which would have occurred had the asset useful lives and residual values remained unchanged.

There was no significant adjustment of asset useful lives and residual values in 2021.

No impairment expense was incurred in the fiscal year 2022.

In 2021 AIXTRON reviewed the valuation of its property, plant and equipment and wrote down (EUR 355 thousand) the value of some specific laboratory equipment that no longer had any economic value.

Assets under construction relates mainly to self-built systems for development laboratories and advanced payments made for the expansion of production and development areas in 2022 and 2021. Prepayments made amount to EUR 6,853 thousand in 2022 (2021:EUR 2,786 thousand).

Disclosures in respect of the underlying leases are shown in note 27.

Other intangible assets include patents, other rights and software.

Amortization and impairment expenses for other intangible assets are recognized in the income statement as follows:

In 2022 an impairment expense of EUR 0 thousand was incurred (2021: EUR 456 thousand). In 2021 impairments were recognized for one IT project that no longer had any economic value and intangible assets in scope of the restructuring of APEVA Group (see also note 28). No reversal of impairment were recognized in fiscal years 2022 and 2021.

At the end of 2022 the Group assessed the recoverable amount of goodwill and determined that as in 2021 no impairment loss had to be recognized.

As at the end of 2022 the cash generating unit, to which the goodwill has been allocated, is the AIXTRON Group Semiconductor Equipment segment.

The recoverable amount of the cash-generating unit is determined through a fair value less cost to sell calculation. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. As AIXTRON has only one cash generating unit (CGU), market capitalization of AIXTRON, adjusted for a control premium, has been used to determine the fair value less cost to sell of the cash generating unit. This is level 2 in the hierarchy of fair value measures set out in IFRS 13.

As at December 31, 2022 the market capitalization of AIXTRON was EUR 3,031 million, based on a share price of EUR 26.97 and issued shares (excluding Treasury Shares) of 112,383,196.

In an orderly selling process costs are incurred. AIXTRON has used 1.5% to account for the costs to sell.

A control premium typically in the range 20% - 40% is incurred in the acquisition of a company. A 20% premium has been applied in this test to adjust the market capitalization to the fair value. Market capitalization was also adjusted for net debt and tax assets prior to comparing it to the carrying amount of the CGU. The analysis shows that the fair value less costs to sell of the CGU AIXTRON exceeds its carrying amount and that Goodwill is not impaired.

The fair value less costs to sell, which is the recoverable amount, exceeds the carrying amount of the CGU by 959% (2021: 797%).

Other non-current financial assets amounting to EUR 705 thousand (2021: EUR 703 thousand) mainly relate to security deposits for buildings.

Deferred tax assets and liabilities are attributable to the following items:

Deferred tax assets are recognized at the level of individual consolidated companies in which a loss was realized in the current or preceding fiscal year, only to the extent that there is convincing evidence that sufficient taxable profit will be available against which the deferred tax assets can be used. The nature of the evidence used in assessing the probability of realization includes forecasts, budgets and the recent profitability of the relevant entity. In fiscal year 2022, deferred tax assets in the amount of EUR 255 thousand (2021: EUR 427 thousand) were recognized, which were attributable to companies that reported a loss in fiscal year 2022 or in the previous fiscal year.

In addition as of December 31, 2022, tax loss carryforwards, temporary differences and tax credits in the amount of EUR 283,072 thousand (2021: EUR 376,931 thousand) existed for which no deferred taxes were recognized.

Of the unrecognized loss carryforwards, temporary differences and tax credits, EUR 233,056 thousand are non-forfeited (2021: EUR 304,134 thousand), EUR 0 thousand expire by 2027 (2021: EUR 0 thousand by 2026) and EUR 50,016 thousand expire after 2027 (2021: EUR 72,797 thousand after 2026).

No deferred tax liabilities were recognized on temporary differences in relation to investments in subsidiaries amounting to EUR 15,470 thousand (2021: EUR 14,144 thousand).

The following table shows the development of deferred tax assets and liabilities during the fiscal year:

The reversal of write-downs recognized during the year in both 2022 and 2021 mainly relates to inventories which had been written down to their net realizable value and subsequently were sold.

Customer-specific work in process relates to work performed at the customers’ site, typically to install equipment or to upgrade customers’ existing equipment. Completion of installation is the final contractual deliverable in most customer contracts which typically allows any remaining payments to be received from the customer.

Additions to allowances against trade receivables are included in other operating expenses, releases of allowances are included in other operating income. Allowances against receivables developed as follows:

Ageing of past due but not impaired receivables:

Due to the worldwide spread of risks, there is a diversification of the credit risk for trade receivables. Generally, the Group demands no securities for financial assets. In accordance with usual business practice for capital equipment however, the Group mitigates its exposure to credit risk by requiring payment by irrevocable letters of credit and substantial payments in advance from most customers as conditions of contracts for sale of major items of equipment.

In 2022 two customers accounted for 11% and 10% of net trade receivables respectively. In 2021 three customers accounted for 28%, 12% and 12% of net trade receivables respectively. In determining concentrations of credit risk, the Group defines counterparties as having similar characteristics if they are part of the same external group of entities.

Included in the Group’s trade receivable balance are debtors with a carrying amount of EUR 17,937 thousand (2021: EUR 2,644 thousand) which are past due at the reporting date for which the Group has not provided. As there has not been a significant change in credit quality, and although the Group has no collateral, the amounts are considered recoverable.

The Group measures the loss allowance for trade receivables at an amount equal to the lifetime expected credit loss. Based on its experience, the Group uses a negligible risk of default for lifetime, adjusted for factors which are specific to the debtors, general economic conditions, and an assessment of both the current as well as the forecast direction of conditions at the reporting date.

In determining receivables which may be individually impaired the Group has taken into account the likelihood of recoverability based on the past due nature of certain receivables, and our assessment of the ability of all counterparties to perform their obligations.

In 2022 other financial assets comprise fund investments. In 2021 other financial assets comprise fund investments as well as bank deposits with maturities with less than 12 months.

The composition of the other financial assets and the maturities at inception of the deposits were as below:

The fair value of fund investments is determined using the quoted prices in active markets at reporting date which is level one of the fair value hierarchy.

Cash and cash equivalents comprise short-term bank deposits with an original maturity of 3 months or less and financial assets that are convertible to cash at any time and are subject to only minor fluctuations in value. The carrying amount and fair value are the same.

No bank balances were given as security either as of the balance sheet date of the fiscal year or in the previous year.

The share capital of AIXTRON SE consists of no-par value shares and was fully paid-up during 2022 and 2021. Each share represents a portion of the share capital in the amount of EUR 1.00.

Authorized share capital, including issued capital, amounted to EUR 169,927,020 (2021: EUR 201,284,934).

Additional paid-in capital mainly includes the premium on increases of subscribed capital as well as cumulative expense for share-based payments.

In 2022 56,400 new shares were issued within the scope of AIXTRON stock option plans (2021: 364,700 shares). 118,881 treasury shares were transferred in 2022 as part of the share-based payments scheme (2021: 0 shares).

A dividend of EUR 0.30 per share was paid in May 2022. Total dividend amount of EUR 33,662 thousand was paid to shareholders of AIXTRON SE (2021: EUR 12,303 thousand).

The Group regards its shareholders’ equity as capital for the purpose of managing capital. In order to ensure the sustainable development of the AIXTRON Group and to maintain the confidence of investors and stake holders, AIXTRON’s capital management aims to maintain a strong capital base. This is also taken into account when determining dividend distributions. The Group considers its capital resources to be adequate.

Income and expenses recognized in other comprehensive income are shown in the state-ment of other comprehensive income.

The foreign currency translation adjustment comprises all foreign exchange differences arising from the translation of the financial statements of foreign subsidiaries whose functional currency is not the Euro.

During 2022 an income of EUR 85 thousand (2021: expense EUR 112 thousand) was recorded from the remeasurement of defined benefit obligations in other comprehensive income.

The calculation of the basic earnings per share is based on the weighted-average number of common shares outstanding during the reporting period.

The calculation of the diluted earnings per share is based on the weighted-average number of outstanding common shares and of common shares with a possible dilutive effect resulting from share options being exercised under the share option plan.

In 2022 and 2021 no share options existed that would be anti-dilutive.

Amounts recognized as distributions to shareholders during the fiscal year and the proposed dividend for the year ended December 31, 2022 are set out in the table below:

The Group grants retirement benefits to qualified employees through various defined contribution pension plans. In 2022 the expense recognized for defined contribution plans amounted to EUR 1,253 thousand (2021: EUR 1,149 thousand).

In addition to the Group’s retirement benefit plans, the Group is required to make contributions to state retirement benefit schemes in the countries in which it operates. AIXTRON is required to contribute a specified percentage of payroll costs to the retirement schemes in order to fund the benefits. The only obligation of the Group is to make the required contributions.

Provisions for defined benefit pension plans in the amount of EUR 115 thousand (2021: EUR 200 thousand) are reported under other non-current provisions.

The Company has different fixed option plans which reserve shares of common stock for issuance to members of the Executive Board, management, and employees of the Group. The Executive Board remuneration system at AIXTRON SE also consists long-term variable remuneration components (long-term incentive, LTI) that are granted in shares of AIXTRON SE.

The fair value of services received in return for shares or stock options granted is measured by reference to the fair value of the equity instruments or stock options granted which are determined using mathematical valuation models.

The fair value of the shares and stock options is determined on the basis of a mathematical model. There were no expenses recognized for the existing program in 2022 and 2021.

In May 2012, options were authorized to purchase shares of common stock. The granted options may be exercised after a waiting period of not less than four years. The options expire 10 years after they have been granted. Under the terms of the 2012 plan, options are granted at prices equal to the average closing price over the last 20 trading days on the Frankfurt Stock Exchange before the grant date, plus 30%. Options to purchase 112,100 common shares were outstanding under this plan as of December 31, 2022.

The amount of long-term performance-related remuneration (LTI) is geared to the perfor-mance of the Group over a 3-year reference period and is granted entirely in AIXTRON shares. Executive Board members may first dispose of these shares following a four-year holding period calculated from the start of the reference period. Before the start of a fiscal year, the Supervisory Board determines the long-term targets for each Executive Board member for the forthcoming reference period. Each Executive Board member receives forfeitable stock awards in the amount of the target LTI as a percentage of the consolidated net income for the year pursuant to the budget adopted for the fiscal year. The number of forfeitable stock awards is calculated based on the average of the closing prices on all stock market trading days in the final quarter of the previous year.

LTI target achievement is determined using the indicators consolidated net income for the year and total shareholder return (TSR), as well as sustainability targets. The TSR is defined as the total shareholder return over the reference period and is calculated as the ratio of the share price development including dividends paid at the end of the reference period to the value at the beginning of the reference period.

In this regard, the relative weighting of the targets amounts to 50% for consolidated net income for the year, 40% for TSR, and 10% for sustainability targets. After the expiry of the three-year reference period, the degree of LTI target achievement is determined by the Supervisory Board. Depending on the degree of target achievement, the forfeitable stock awards are then converted into vested stock awards or otherwise lapse. The maximum number of vested stock awards that may be granted in connection with LTI is capped at 250% of the number of forfeitable stock awards granted at the start of the reference period.

The shares are transferred to the Executive Board member after the four-year restriction period.

The fair value of equity-settled share-based payment transactions is recognized as an expense over the vesting period and a corresponding adjustment is made to equity. The fair value of the shares granted is measured based on a valuation model taking into account the vesting conditions at which the shares are granted. The calculation takes into account estimates for future dividends. The TSR ratio is used as a market condition in estimating the fair value at the valuation date. For the other non-market-based vesting conditions, the Group reviews its estimate of the number of equity instruments during the vesting period. Adjustments in the original estimates, if any, are recognized in profit or loss and a corresponding adjustment is made to equity.

The following table shows the main parameters of the valuation model (Monte Carlo simulation) for the long-term variable remuneration of the Executive Board (LTI) for the LTI Tranche 2022 and 2021:

In 2021 there were two grant dates each, due to a later entry date of an Executive Board member. Assumptions regarding volatility and correlation between the AIXTRON share and the Peer Group were determined based on historical share price developments.

Within the scope of the LTI Tranche 2022 224,941 forfeitable share awards were granted with the weighted average fair value of EUR 17.35 per award on grant date (LTI Tranche 2021: 177,930 forfeitable share awards with the weighted average fair value of EUR 15,54 per award). At the end of the reference period, the forfeitable share awards of LTI Tranche 2022 or 2021 are converted into vested stock awards or partially forfeited.

In 2022, the personnel expenses from share-based payments, all of which were equity settled share-based payments, were EUR 4,441 thousand (2021: EUR 3,860 thousand). Share-based payments include the expense of long-term incentive of the Executive Board which is paid in shares (see note 31).

Development and breakdown of provisions:

These include mainly provisions for holiday pay, payroll, severance payments and other variable element of pay, which are financial liabilities.

These include provisions associated with contracts where the unavoidable costs of meeting the contract obligations exceed the economic benefits expected to be received. These mainly relate to supply contracts for materials which are excess to the forecast future requirements.

Warranty provisions are the estimated unavoidable costs of providing parts and service to customers during the normal warranty periods.

Other provisions consist mainly of the estimated cost of services received and also include pension provisions.

For provisions existing at both December 31, 2022 and December 31, 2021, the economic outflows resulting from the obligations that are provided for are expected to be settled within one year of the respective balance sheet date for current provisions and within two years of the respective balance sheet date, but more than one year, for the main non-current provisions (excluding pension provisions).

The liabilities consist of the following:

The carrying amount of trade payables and other current liabilities approximates their fair value. Trade payables, grant liabilities, taxes and other liabilities fall due for payment within 34 days of receipt of the relevant goods or services.

Short-term lease liabilities are explained in note 25.

Details of the significant accounting policies and methods, the basis of measurement that are used in preparing the financial statements and the other accounting policies that are relevant to an understanding of the financial statement are disclosed in note 2 to the financial statements.

The Group seeks to minimize the effects of any risk that may occur from any financial transaction. Key aspects are the exposures to liquidity risk, credit risk, interest rate risk and currency risk arising in the normal course of the Group’s business.

The AIXTRON Group’s central management coordinates access to domestic and international financial institutions and monitors and manages the financial risks relating to the operations of the Group through internal risk reports which analyze exposure to risk by likelihood and magnitude. These risks cover all aspects of the business, including financial risks.

Liquidity risk is the risk that the Group is unable to meet its existing or future obligations due to insufficient availability of cash or cash equivalents. Managing liquidity risk is one of the central tasks of AIXTRON SE. In order to be able to ensure the Group’s solvency and flexibility at all times cash and cash equivalents are projected on the basis of regular financial and liquidity planning.

As of December 31, 2022 the Group did not have any borrowings (2021: nil). Financial liabilities, all due within one year, of EUR 52,679 thousand (2021: EUR 26,018 thousand) consisting of trade payables and other liabilities and are shown in note 24, together with an analysis of their maturity. Non-current payables consist of lease liabilities and other payables. Long term lease liabilities of EUR 5,874 thousand (2021: EUR 3,052 thousand) are shown with an analysis of their maturity in note 27. Other non-current payables of EUR 101 thousand (2021: EUR 244 thousand) are due after more than one year.

As of December 31, 2022 the Group had EUR 325,411 thousand (2021: EUR 352,694 thousand) of bank deposits and investments as described in notes 13, 17 and 18.

Financial assets generally exposed to a credit risk are trade receivables, financial investments, and cash and cash equivalents.

The Group’s cash and cash equivalents and financial investments are kept with financial institutions that have a good credit standing. Central management of the Group assesses the counter-party risk of each financial institution dealt with and sets limits to the Group’s exposure to those institutions. These credit limits are reviewed from time to time so as to minimize the default risk as far as possible and to ensure that concentrations of risk are managed.

The maximum exposure of the Group to credit risk is the total amount of receivables, financial assets and bank deposits as described in notes 13, 16, 17 and 18.

For contract assets measured at fair value, the maximum amount of the exposure to credit risk is the amount of contract assets measured at fair value as disclosed in note 25. There are no credit derivatives or similar instruments which mitigate the maximum exposure to credit risk and there has been no change during the period or cumulatively in the fair value of such receivables that is attributable to changes in the credit risk.

The Group’s activities expose it to the financial risks of changes in foreign currency exchange rates and interest rate risks. Interest rate risks are not material as the Group only receives a minor amount of interest income. The Group does not use derivative financial instruments to manage its exposure to interest rate risk. Cash deposits are made with the Group’s bankers at the market rates prevailing at inception of the deposit for the period and currency concerned. The Group’s financial investments are made into funds bases in the European Union and are exposed to changes in the market value of those funds. There has been no change to the Group’s exposure to market risk or the manner in which it manages and measures the risk.

The Group can enter into a variety of derivative financial instruments to manage its exposure to foreign currency risk, including forward exchange contracts to hedge the exchange rate risk arising on the export of equipment. The main exchange rates giving rise to the risk are those between the US Dollar, GB Pound, Chinese Renminbi and Euro. No forward exchange contracts were entered into in the fiscal year or in the previous year.

The carrying amounts of the Group’s foreign currency denominated monetary assets and monetary liabilities at the reporting date are as follows:

Exposures are reviewed on a regular basis and are managed by the Group through sensitivity analysis.

The Group's global operations expose it primarily to foreign exchange risks by the US Dollar, GB Pound and Chinese Renminbi.

The following table details the Group’s sensitivity to a 10% change in the value of the Euro against the US Dollar, GB Pound and Chinese Renminbi. A positive number indicates an increase in profit, a negative number indicates a reduction in profit.

The sensitivity analysis represents the foreign exchange risk at the year-end date only. It is calculated by revaluing the Group's financial assets and liabilities, existing at 31 December, denominated in US Dollars, GB Pounds or Chinese Renminbi by 10%. It does not represent the effect of a 10% change in exchange rates sustained over the whole of the fiscal year, only the effect of a different rate occurring on the last day of the year.

Cash and cash equivalents, receivables are stated at amortized cost. Other financial assets in 2022 and 2021 comprise financial assets measured at FVTPL. Contract assets are outside the scope of IFRS 9.

For trade receivables/payables due within less than one year, measured at amortized cost, the fair value is equivalent to the carrying amount.

* For the financial assets and financial liabilities at amortized cost the carrying amount is a reasonable approximation of fair value.

Contract liabilities for advance payments from customers occur when a contract requires the customer to pay a deposit to the Group and the deposit has actually been paid, typically near the commencement of the contract, or if it reflects an unconditional payment claim. Usually, advance payments are up to 50% of the total contract price.

The Group records the liability as the advance payment is received and eliminates the liability at the same time and up to the same amount as it records revenue until the liability is fully extinguished. Changes in contract liabilities for advance payments in the year reflect the changing level of outstanding customer orders.

Revenues of EUR 60,821 thousand were realized in 2022 from the EUR 77,041 thousand of contract liabilities for advance payments outstanding at the end of 2021. Revenues of EUR 40,728 thousand were realized in 2021 from the EUR 50,824 thousand of contract liabilities for advance payments outstanding at the end of 2020. In 2022 no revenue was recognized from performance obligations that were settled in prior years.

The undiscounted lease liabilities are payable as follows:

Note 11 includes the disclosures required by IFRS 16 concerning the depreciation charge for leased assets by underlying class of asset, additions to leased assets and the carrying value of leased assets at the end of the reporting period.

The Group has applied paragraph 6 of IFRS 16 when accounting for short-term leases and low-value leases and has expensed these on a straight-line basis. A similar portfolio of short-term leases exists at the reporting date.

The Group leases certain buildings, equipment and vehicles under various leases. Under most of the lease commitments for buildings the Group has options to renew the leasing contracts. The leases typically run for a period between one and ten years. None of the leases include contingent rentals.

No restructuring costs had to be incurred in the fiscal year 2022.

In the previous year, the restructuring of the Group's OLED activities resulted in expenses of EUR 3,888 thousand. These mainly related to compensation payments, other personnel-related expenses, and impairment losses.

Expenses incurred in the following areas:

AIXTRON is occasionally involved in legal proceedings or can be exposed to a threat of legal proceedings in the normal course of business. The Executive Board regularly analyses these matters, considering any possibilities of avoiding legal proceedings or of covering potential damages under insurance contracts and has recognized, where required, appropriate provisions. It is not expected that such matters will have a material effect on the Group’s net assets, results of operations and financial position.

The related parties of AIXTRON SE are the fully consolidated subsidiaries according to note 32.

Related parties of the Group are members of the Executive Board and members of the Supervisory Board and their close relatives.

SBG Beteiligung GmbH is also a related party because the company is controlled by a related person of AIXTRON SE. There were no transactions with AIXTRON in the fiscal year or in the previous year.

The disclosures of key management personnel compensation are as follows:

Share-based payments refer to the fair value of share options at grant date and includes that portion of bonus agreements which is settled in shares.

The target expense for the share-based payments of the Executive Board planned at the grant date amounted to EUR 3,902 thousand for the fiscal year (2021: EUR 2,766 thousand) (which corresponds to the remuneration granted).

Individual amounts and further details regarding the remuneration of the members of the Executive Board and Supervisory Board are disclosed in the Remuneration Report.

AIXTRON SE controls the following subsidiaries:

All companies in the Group are engaged in the supply of equipment to the semiconductor industry or development facilities. Design and manufacture of equipment takes place at the entities in Germany and Great Britain. Service and distribution take place at all locations.

There are no events which have occurred after the balance sheet date, of which the directors have knowledge, which would result in a different assessment of the Group’s net assets, results of operation and financial position.

Fees expensed in the income statement for the services of the Group auditor, KPMG AG Wirtschaftsprüfungsgesellschaft, Essen (2021: Deloitte GmbH Wirtschaftsprüfungsgesellschaft, Düsseldorf) are as follows:

The fees for other confirmation services include fees for audits of the non-financial Group report (2021: fees for audits in accordance with EEG, KWKG and the non-financial Group report).

Compared to last year, the average number of employees during the current year was as follows:

Membership of Supervisory Boards and Controlling Bodies:

Membership of Supervisory Boards and Controlling Bodies:

Membership of Supervisory Boards and Controlling Bodies:

Membership of Supervisory Boards and Controlling Bodies:

Membership of Supervisory Boards and Controlling Bodies:

The composition of the Company’s Executive Board in 2022 is:

The preparation of AIXTRON’s Consolidated Financial Statements requires management to make certain estimates, judgments, and assumptions that the Group believes are reasonable based upon the information available. These estimates and assumptions affect the reported amounts and related disclosures and are made in order to fairly present the Group’s financial position and results of operations. The following accounting policies are significantly impacted by these estimates and judgments that AIXTRON believes are the most critical to aid in fully understanding and evaluating its reported financial results:

Revenue for the supply of most equipment to customers is generally recognized in two stages, partly on delivery and partly on final installation and acceptance (see note 2 (N)). When allocating the transaction price to the two performance obligations, delivery of the tool and installation of the tool, assumptions are made regarding individual margins as part of the cost-plus method. The Group believes, based on past experience, that this method of recognizing revenue fairly states the revenues of the Group. For the reporting periods 2022 and 2021, 10% of the installation revenue was allocated to installation performance.

The judgements made by management include an assessment of the point at which control has passed to the customer.

Inventories are stated at the lower of cost and net realizable value. This requires the Group to make judgments concerning obsolescence of materials. This evaluation requires estimates, including both forecasted product demand and pricing environment, both of which may be susceptible to significant change. The carrying amount of inventories and details on impairment losses and reversals of impairment losses in the fiscal year are disclosed in notes 3 and 15. In future periods, impairment losses may be necessary due to various factors such as decreasing product demand or technological obsolescence. These factors could result in adjustment to the valuation of inventory in future periods, and significantly impact the Group’s future operating results

At each balance sheet date, the Group assesses whether the realization of future tax benefits is sufficiently probable to recognize deferred tax assets. This assessment requires the exercise of judgement on the part of management with respect to future taxable income. The parent company AIXTRON SE does generally not exceed a planning horizon of twelve months. The recorded amount of total deferred tax assets could be reduced or increased if estimates of projected future taxable income are lowered or increased, or if changes in current tax regulations are enacted that impose restrictions on the timing or extent of the Group’s ability to utilize future tax benefits. The carrying amount of deferred tax assets is disclosed in note 14.

Provisions are liabilities of uncertain timing or amount. At each balance sheet date, the Group assesses the valuation of the liabilities which have been recorded as provisions and adjusts them if necessary. Because of the uncertain nature of the timing or amounts of provisions, judgement has to be exercised by the Group with respect to their valuation. Actual liabilities may differ from the estimated amounts. Details of provisions are shown in note 23.

In the normal course of business, the Group is subject to various legal proceedings and claims. The Company, based upon advice from legal counsel, believes that the matters the Group is aware of are not likely to have a material adverse effect on its financial condition or results of operations. The Group is not aware of any unasserted claims that may have a material adverse effect on its financial condition or results of operation.

The global impact of the Corona pandemic and the Russia/Ukraine conflict on business operations is explained in the combined management report. The impact on the 2022 consolidated financial statements is immaterial and it is also expected that the impact on fiscal year 2023 will be immaterial. Climate risks also did not have a material impact on the business operations of AIXTRON.

The current Declaration of Conformity according to section 161 German Stock Corporation Act (“Aktiengesetz”), which was adopted by the Executive Board and the Supervisory Board in February 2023, is permanently available on AIXTRON's website under Investors/Corporate Governance.

Herzogenrath, February 27, 2023

AIXTRON SE

Executive Board

Alan Tai

Taiwan/Singapore

Christof Sommerhalter

USA

Christian Geng

Europe

Hisatoshi Hagiwara

Japan

Nam Kyu Lee

South Korea

Wei (William) Song

China

AIXTRON SE (Headquarters)

AIXTRON 24/7 Technical Support Line

AIXTRON Europe

AIXTRON Ltd (UK)

AIXTRON K.K. (Japan)

AIXTRON Korea Co., Ltd.

AIXTRON Taiwan Co., Ltd. (Main Office)

AIXTRON Inc. (USA)

Christoph Pütz

Senior Manager ESG & Sustainability

Christian Ludwig

Vice President Investor Relations & Corporate Communications

Ralf Penner

Senior IR Manager

Christian Ludwig

Vice President Investor Relations & Corporate Communications

Prof. Dr. Michael Heuken

Vice President Advanced Technologies